Analysis of an Audit

Financial Audit Reports

Our two main financial audits are mandated by State and/or federal laws. They are:

-

State of Michigan Annual Comprehensive Financial Report Audit

Statewide Single Audit

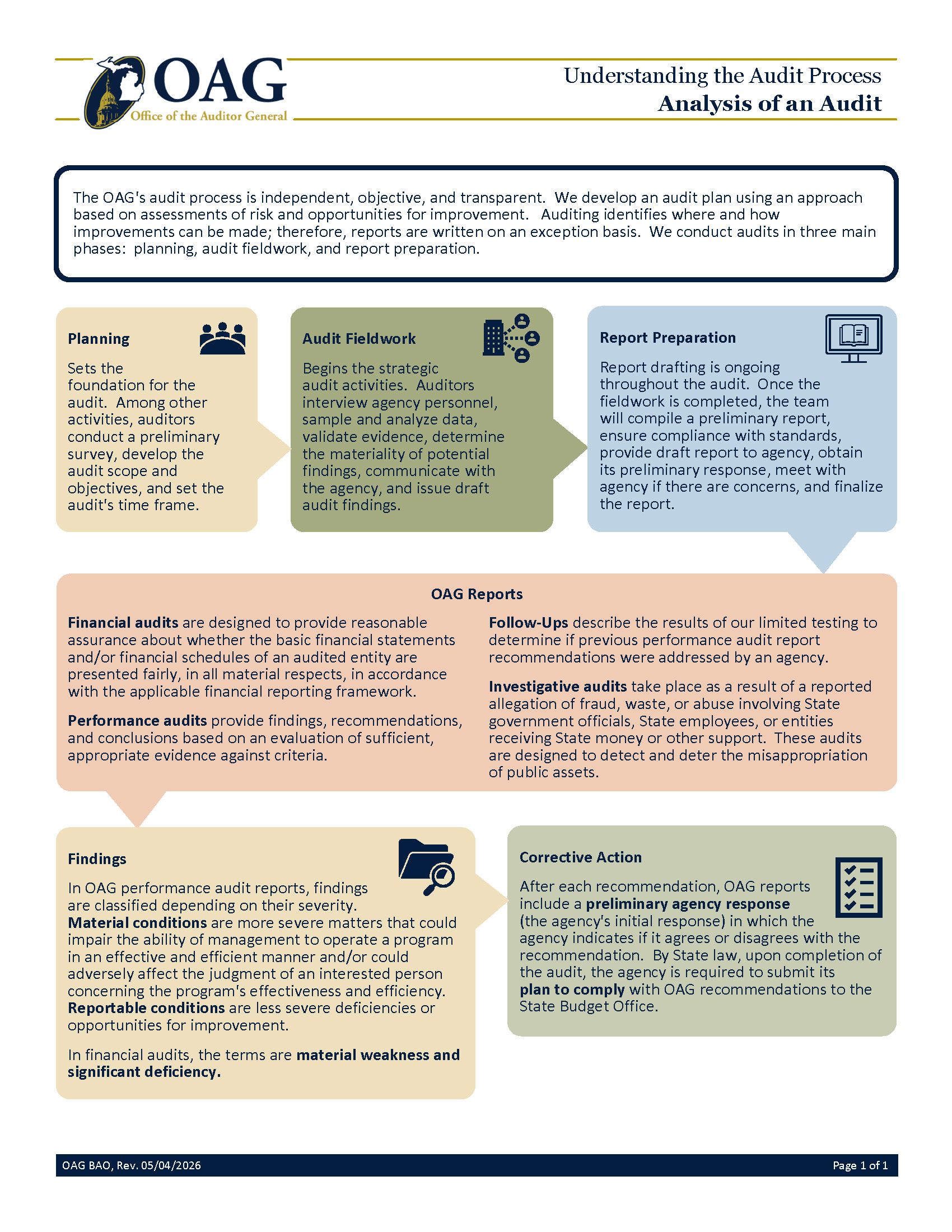

We develop our audit plan using an approach based on assessments of risk and opportunities for improvement.

We focus audit efforts on the activities identified through a preliminary survey that we believe have the greatest probability for improvement and/or the most significant consequences if proper execution does not occur.

Auditing identifies where and how improvements can be made; therefore, audit reports are written on an exception basis. Stated another way, we typically do not continue audits if the program appears to function as intended; our resources are more impact-driven if we focus on areas for improvement.

We focus audit efforts on the activities identified through a preliminary survey that we believe have the greatest probability for improvement and/or the most significant consequences if proper execution does not occur.

Auditing identifies where and how improvements can be made; therefore, audit reports are written on an exception basis. Stated another way, we typically do not continue audits if the program appears to function as intended; our resources are more impact-driven if we focus on areas for improvement.

Generally, we conduct audits in three main phases:

-

Planning Phase

This phase sets the foundation for the audit and includes conducting a preliminary survey, brainstorming, conducting research, developing the audit scope and objectives, setting the audit’s time frame, and performing many other activities. In this phase, we:

- Review organization structure.

- Review applicable State and federal laws.

- Research legislation impacting the audited program.

- Understand how the auditee strives to reach its mission, goals, policies, and procedures.

- Review agency-produced reports.

- Identify relevant criteria to audit against, such as best practices, benchmarks, and audits of similar entities and from other states.

-

Audit Fieldwork Phase

This phase begins the strategic audit activities. During audit fieldwork, we:

- Interview agency personnel.

- Sample and analyze data.

- Issue surveys if applicable.

- Validate evidence.

- Determine materiality of potential findings.

- Communicate with the agency.

- Issue draft audit findings.

-

Report Preparation Phase

This phase is the final stage of the audit. At this time, we:

- Draft the preliminary report.

- Ensure compliance with auditing standards.

- Ensure compliance with internal quality standards.

- Provide the agency with draft report.

- Obtain the agency preliminary response.

- Meet with the agency to address its concerns.

- Finalize the report.

- Release the report.

Agency Preliminary Response

In each audit report containing findings, we include the agency's initial response (i.e., agency preliminary response) in which the agency indicates if it agrees, partially agrees, or disagrees with the recommendation(s) and its plan to comply.

Plan to Comply

By State law, upon completion of an audit, the agency is required to submit its plan to comply with the recommendations to the State Budget Office, which either accepts the plan as final or contacts the agency to take additional steps to finalize it. Our website includes the final plan to comply following each audit report.

In each audit report containing findings, we include the agency's initial response (i.e., agency preliminary response) in which the agency indicates if it agrees, partially agrees, or disagrees with the recommendation(s) and its plan to comply.

Plan to Comply

By State law, upon completion of an audit, the agency is required to submit its plan to comply with the recommendations to the State Budget Office, which either accepts the plan as final or contacts the agency to take additional steps to finalize it. Our website includes the final plan to comply following each audit report.

Generally accepted auditing standards of the American Institute of Certified Public Accountants.

Government Auditing Standards issued by the Comptroller General of the United States.

Title 2, U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance)

Government Auditing Standards issued by the Comptroller General of the United States.

Title 2, U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance)

Yes, the Government Auditing Standards requires a triennial peer review of our operations . The peer review is performed by a multi-person National State Auditors Association external quality control review team. We have received thirteen consecutive unmodified “clean” opinions. This is the highest level of opinion.

The Auditor General for the State of Michigan is appointed by the Legislature, as prescribed by Article IV, Section 53 of the Michigan Constitution. Doug Ringler, CPA, CIA, was reappointed Auditor General by the Michigan Legislature on May 26, 2022 for a second eight-year term by the Senate Concurrent Resolution No. 27 of 2022.

Yes, the Auditor General is nonpartisan and independent. Article IV, Section 53 of the Michigan Constitution organized the OAG in the legislative branch of State government to conduct audits of State government operations.

The Auditor General conducts post-audits of State government agencies and operations per the Michigan Constitution. See also the Audits and Examinations Act and Attorney General Opinion 6749.

The OAG cannot audit local governments, school districts, private businesses, or individual taxpayers. This limit is set forth by the Michigan Constitution and Attorney General Opinion 6225, Attorney General Opinion 6970, and Attorney General Opinion 7158.

If you have a concern about an entity that we cannot audit, you may find the following resources helpful:

• Department of Treasury Bureau of Local Government

• Michigan Municipal League

If you have a concern about an entity that we cannot audit, you may find the following resources helpful:

• Department of Treasury Bureau of Local Government

• Michigan Municipal League

The OAG has no enforcement authority for corrective action. The OAG provides the information to the audited agency, the Legislature, and the public. The auditee is required to establish a corrective action plan. The Legislature may request the OAG to present an audit report at a public meeting and request the agency to present its response and corrective actions. The executive branch has the authority to make changes through policy, procedure, or rule, and the Legislature has the authority to effect change through State law or State appropriations.

The OAG may follow up on the status of previously reported findings and issue a Follow-Up Report on Prior Audit Recommendations to the public with the results. Follow-ups are often performed for material findings within an 18-month window at the discretion of the Auditor General based on resources and other factors, such as the amount of time that an agency may reasonably need to make changes.

The OAG may follow up on the status of previously reported findings and issue a Follow-Up Report on Prior Audit Recommendations to the public with the results. Follow-ups are often performed for material findings within an 18-month window at the discretion of the Auditor General based on resources and other factors, such as the amount of time that an agency may reasonably need to make changes.

The Work in Progress tab of our website contains the audit objective(s) and estimated report release dates for all ongoing audits. The tab is located at the top of our website home page.

Yes, you may sign up here and receive an e-mail for every report issued by the Auditor General. The OAG also notifies interested parties when projects begin and when a date has been established for a report release. In addition, the OAG includes links to the reports once released via X (formerly known as Twitter), LinkedIn, and Facebook. You may choose to follow us on one or more of those mediums and receive our posts.

Reports are issued to the audited agency, to all legislators, and to the public. Anyone can find the reports on our website, ask to be on our e-mail distribution list, and follow us on X (formerly known as Twitter), LinkedIn, or Facebook, where we post all report links at the time of release.

To contact the OAG with a concern, you can use the Contact Us or or the Fraud/Waste/Abuse Allegation Form links located to these forms can be found at the bottom of our website home page.